Tom: Good morning, everyone, and welcome to our webinar on “Payday Super’s Here: What Employers Need to Know About the New Rules.”

My name is Tom Linnane, and I’m a senior lawyer in LegalVision’s tax team.

Before we begin, a couple of quick housekeeping items. You’ll receive the recording and slides in your email after the webinar is over.

Please submit your questions in the Q&A box, and we’ll answer them at the end of the webinar. Please complete the feedback survey after the webinar is over, and stay until the end to enter our Apple AirPods monthly draw.

By viewing this webinar, you qualify for a complimentary consultation with LegalVision to discuss how we can help your business. To claim, leave your details in the survey that appears when the webinar ends, or contact us via our website.

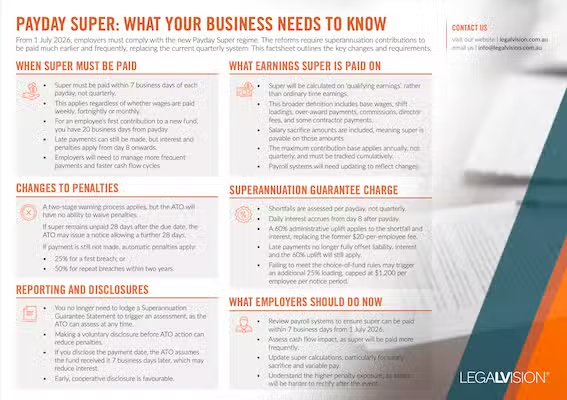

This factsheet outlines the key changes and requirements under the reforms, which require superannuation contributions to be paid earlier and more frequently instead of quarterly.

Overview of Topics

Tom: So today, we’ll be discussing:

- When superannuation must now be paid under the payday superannuation laws.

- What earnings superannuation is now paid on.

- Changes to the superannuation penalties regime.

- How the superannuation guarantee charge is changing.

- Updates to reporting and disclosure obligations.

- Practical tips for employers to implement the new rules moving forward, and then we’ll finish up with some Q&A.

When Superannuation Must Be Paid

Tom: Now, I’ll start with the changes regarding when superannuation must be paid. Right now, an employer has 28 days from the end of the quarter to make contributions to their employees’ superannuation funds for those contributions to be considered on time.

Perhaps the most significant change under the payday super laws is how this is changing. Employers will now have 7 business days from payday to make the contributions for them to be considered on time.

It’s really important to remember that the contribution time is when the fund actually receives the money, not when the amount is actually paid by the employer.

This should be kept in mind when making contributions, particularly around weekends and public holidays, which can cause delays in the transfer times between when the employer pays the money and when the fund receives it.

One exception to the 7 business day rule is if the contribution is the employer’s first contribution to a new fund. In that case, the due date is 20 business days from payday.

Late payments can still be made, but interest and penalties will apply from day 8 onwards. That’s important to remember.

Superannuation on Qualifying Earnings

Now, let’s talk about what superannuation must actually be paid on in terms of earnings.

Previously, superannuation contributions were calculated based on an employee’s ordinary time earnings if the payment was made on time, or the employee’s salary or wages if it was late, with some discrete differences between the two.

This is shifting to the amount of qualifying earnings paid to an employee on each QE day, with QE day essentially being the date that the employer pays the employee’s salary or wages.

Qualifying earnings includes the concept of ordinary time earnings, but also expands the scope by directly including all commission payments and any amounts that an employee’s salary or wage is reduced under a salary sacrifice agreement.

Employers will need to ensure that whatever payroll systems they’re using are set up to capture the wider definition of qualifying earnings.

Maximum Contribution Base

Another change under the payday super laws is how the maximum contribution base will no longer be tracked quarterly, but instead will be tracked per financial year.

For those who are unfamiliar, the maximum contribution base is the capped ordinary time earnings, which will now be qualifying earnings, that an employee is taken to have been paid for the purposes of calculating superannuation contributions. This caps the employer’s superannuation contributions for high-income earners.

This means that employees will need to keep track of payments made to high-income earners across the financial year instead of quarterly to determine whether an employee has already reached the maximum contribution base for that year.

Changes to the Superannuation Guarantee Charge

So now let’s move on and talk about how the superannuation guarantee charge has changed. Under the old system, if you had a shortfall for a quarter, you calculated the superannuation guarantee charge at the end of that quarter based on the total wages you paid over that last three-month period.

Under the new system, every time you pay wages to an employee, being that employee’s QE day, you have an individual superannuation obligation on that specific payday for that specific employee. If you don’t meet it, a shortfall arises immediately for that payday.

This means that you could, in theory, have multiple shortfalls in a single month if you miss payments, rather than one shortfall per quarter.

Changes to the Components of the Charge

The components of the charge have also changed. Under the old system, the superannuation guarantee charge was made up of three parts: the actual shortfall amount, an interest component, and an admin fee.

Under the new rules, your total charge for each QE day now includes the individual final shortfall (or the super you didn’t pay), minus any late contributions, a notional earnings component, which is a daily interest amount that accrues from day 8 after payday until you pay, or the ATO assesses you, and an administrative uplift, which is up to 60% on top of your shortfall, plus the interest component.

There’s also a potential 25% choice loading if you didn’t comply with the choice of fund rules. This 25% loading is capped per employee.

Administrative Uplift

The 60% administrative uplift is the big change here, which we’ll talk about on the next slide.

Under the old system, the admin component was about $20 per employee per quarter. So, let’s just say you had a $1,000 shortfall per employee for one employee for the quarter, you’d pay roughly $1,020 plus interest.

Under the new system, that same $1,000 shortfall attracts 60% on top, so you’d be paying $1,600 plus interest.

And that 60% also applies to the interest itself.

This uplift cannot be waived or reduced by the ATO, although we expect that regulations will be made which could allow reductions for early voluntary disclosure.

No Offset Mechanism Under the New System

What an employer can do is reduce the amount they may have to ultimately pay through late payments. Under the old system, if you made a contribution after the 28-day deadline but before the ATO assessed you, you could elect to offset the late payment against the charge, which would reduce your nominal interest component and then your shortfall.

Under the new system, there’s no offset mechanism anymore. However, contributions made within the 7 business day window (or 20 business days for first contributions to a new fund) completely eliminate your shortfall. Contributions made after those dates, but before your assessment, would reduce your final shortfall to zero, but you still pay the notional interest amount and the uplift on that interest amount.

With interest accruing daily from day 8.

Interest Calculations

Whereas under the old system, interest was calculated from the start of the quarter to when the charge became payable, so it was a set period. Under the new system, interest accrues every single day from day 8 after payday until you pay the amount, or the ATO assesses you.

This means that the longer you delay, the more interest compounds, and the 60% uplift will apply to all of that accumulated interest.

Reporting and Disclosures

So, moving on to the next slide, let’s talk about reporting and disclosures. Reporting a shortfall is now no longer compulsory. Under the old system, you were legally required to lodge a superannuation guarantee statement if you had a shortfall for a quarter, with specific deadlines for each quarter. Failure to lodge triggered certain penalties.

Under the new system, lodging a statement is completely voluntary, and there’s no penalty for choosing not to report, because the penalty regime now focuses more on non-payment rather than non-reporting.

However, it’s important to bear in mind that the ATO can still assess you at any time based on their own data, such as through single-touch payroll, fund contribution data, and employee complaints.

So, it doesn’t mean that voluntary disclosure is optional for paying, it’s just that there’s no penalty for not making that voluntary disclosure.

Voluntary Disclosures Can Still Be Valuable

But, if we move on to the next slide, I will talk through how, despite voluntary disclosures no longer being mandatory, they can still be strategically valuable for a business.

A big part of this is the payment day deeming rule, which can reduce the interest charges that may ultimately be applied.

So, if you lodge a voluntary disclosure and include when you paid a contribution (but not necessarily when it had to have been received by the fund), the ATO will deem that the fund received it 7 business days after you lodged the voluntary disclosure.

This can help when you don’t have evidence of the exact receipt date of the fund receiving that money, or if the fund took longer than 7 days to process the payment.

For example, if you make a payment on day 3 after payday but can’t prove when the fund actually received it, by disclosing the payment date on day 3, the ATO would deem receipt on day 10 (day 3 plus 7 business days). This could save you a lot of interest if the actual receipt happened much later, or if the fund processed it later.

Importance of Voluntary Disclosure

It’s also expected that, as I said earlier, the legislation allows for regulations to be made, which could reduce the 60% administrative uplift if a voluntary disclosure is made. But this is something we’ll have to keep an eye on for the time being.

That said, and this applies to many tax matters generally, voluntarily disclosing tax liability shortfalls shows that you’re being proactively compliant with the ATO. Even though it doesn’t necessarily affect assessment or penalties, it shows good faith, which matters if you’re seeking alternative payment arrangements with the ATO or if you ultimately end up in a dispute with them.

The ATO is usually more favourable towards taxpayers who have historically shown good compliance or at least a willingness to engage with them, rather than those who ignore the issue.

We appreciate your feedback – your submission has been successfully received.