Laini Bennett: Hello and welcome, everyone, to our webinar on how the 2026 budget impacts your business.

My name is Laini Bennett, and I’m pleased to welcome our co-host for today. Our expert speakers are Thomas Linnane, who is our Senior Tax Lawyer for LegalVision, and James Carey, Director for accounting firm Prime Partners. Welcome to both of you.

Before we begin, a couple of quick housekeeping items.

You will receive a copy of the recording from today, so if you don’t want to take copious notes, rest assured, the recording will be coming.

We are sure you’re going to have lots of questions, so please submit them in the Q&A box that appears in your toolbar, and after we get through the body of the discussion, we will address your questions then.

We do have a feedback survey after the webinar, and we’d love to hear from you so that we can continue to improve the quality of our webinar offering. And if you stick around to the end of the webinar, you can go into our draw for Apple AirPods.

So, as I said, you’re likely to have many questions about the budget’s impact, and the good news is that by watching this webinar, you’re eligible for a complimentary consultation with LegalVision. You’re going to receive a call from our team this week, and we’ll discuss with you how we can help your business to resolve its legal issues.

So, today we have got quite a lot on the agenda. We’re going to be talking about the key budget impacts for businesses, and we’re also addressing your end of financial year obligations. I might just add that when we first set up this webinar, originally the webinar was about the end of financial year, but the budget came out last week, and the amount of questions coming through was overwhelming, so we decided to pivot and focus on the budget. But we will, as I say, address your end of financial year obligations. We’re going to kick off today’s discussion with CGT reforms, before moving on to discretionary trusts. We’ll talk about business tax wins and R&D incentives and startup concessions. We’ll then move on to the end of financial year obligations and planning. And of course, a few key takeaways for you and your Q&A opportunities.

So, without further ado, let’s get started with our discussion. Last week, the budget was handed down, and the changes were very controversial and significant.

So, Tom, to put it mildly, CGT changes are getting a lot of attention. For business owners holding company shares, commercial property, goodwill, or other business assets, what could these reforms change when they’re considering selling, restructuring, or bringing in investors?

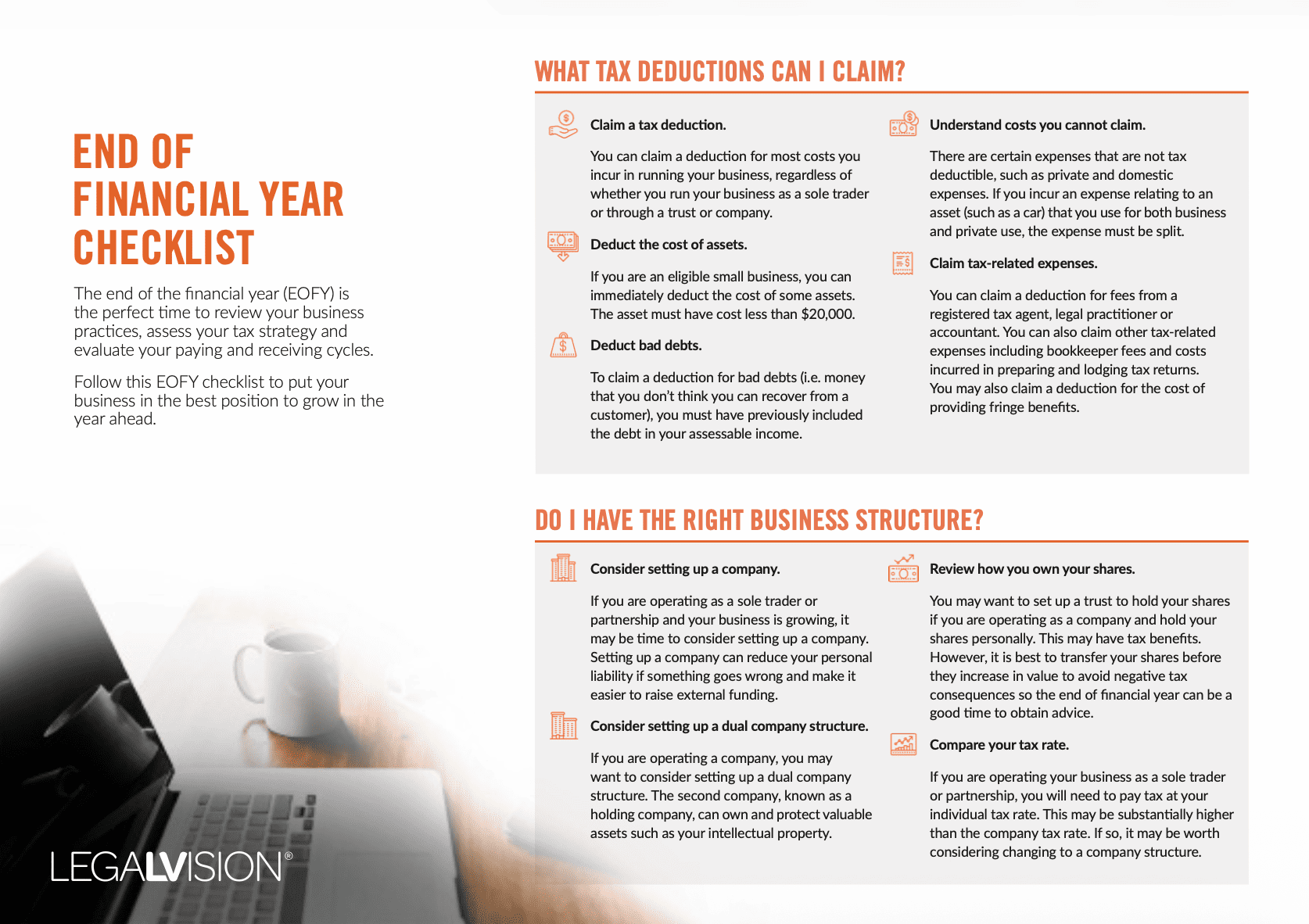

The end of the financial year (EOFY) is the perfect time to review your business practices, assess your tax strategy and evaluate your paying and receiving cycles.

This checklist outlines:

+ the tax deductions your business can claim;

+ whether you have the right business structure; and

+ how to chase up late payments.

Thomas Linnane: Great, thanks, Laini. So, look, to start by addressing the elephant in the room, while the changes to the CGT discount are a pretty significant shift, it’s not the automatic 47% tax, like the memes featuring Anthony Albanese are suggesting, but it is quite a shift away. So, instead of individuals and trusts getting an automatic 50% discount on any CGT asset, which can include things like shares, property, a range of assets, has been replaced with adjusting the cost base of that asset based on CPI, Consumer Pricing Index, and a minimum 30% tax.

So, it could shift things quite a bit, and what founders in particular, but also businesses that are considering selling their assets, will need to think about in the lead-up to when these changes kick in on the 1st of July 2027, is whether they do want to look at, say, an early exit or an early sale of those assets to really capitalise on the CGT discount while it is available.

Or otherwise, thinking about what they do around 1 July 2027, thinking about whether or not they get a valuation to actually look at what their gain would be moving forward on that particular asset, given that the changes really only are to capture gains on those assets from 1 July 2027. So there’s a bit of planning that’ll need to happen, a lot of discussions with tax advisors to figure out what the exit plans are for people who are looking for an exit in the future, and what the potential tax impact might be.

But then this is overlaid, I guess, with whether or not we look in more detail at other concessions which might be available, which aren’t being affected by the CGT discount reforms. So things like the small business CGT concessions, which can allow a capital gain to be reduced or disregarded in certain circumstances. So I think moving forward, those concessions are going to be given a lot more attention and trying to be utilised by a wider range of taxpayers moving forward.

And then other concessions, more specifically in the investment space, given that, at least at face value, you could make the argument that maybe investing in startups and companies maybe won’t be attractive anymore, given the discount is being altered. Things like the Early Stage Innovation Company concession, which is available to investors who invest in early-stage innovative companies, is probably going to become a lot more attractive.

And so that concession, if it’s available, can allow an investor to completely disregard any capital gain that they make as a result of selling those shares that they get in those companies, provided they’ve held those shares for a certain period of time. So, I think it’s two-fold: it’s looking at exit strategies and planning around how those potential exits and sales of assets are going to be managed, but also looking at those other concessions in a bit more detail to try and make those investments and exits still as attractive as possible.

Laini Bennett: You mentioned startups and the impacts on startups. There’s been a lot of talk about whether the CGT changes will drive startups overseas to countries like New Zealand and Singapore, where there’s no CGT.

So, how could the CGT changes, if they go in as currently outlined, affect founder equity, employee share scheme option plans, and startup concessions?

Thomas Linnane: Yeah, there has been a lot of discussion around these potential impacts on the startup space, and I would start by saying that the government has committed to having consultation with the startup sector over the next couple of weeks, I believe, to discuss the proposed CGT changes and how it may impact the startup space.

So, at this stage, it’s a bit of a wait and see to see if there’s any carve-outs or any relief that eligible startups or even small businesses might get from these proposed changes. Because, arguably, these incentive plans a lot of startups put in place whereby their employees receive options or shares in the company in exchange for their services, with the idea being that those companies generally can’t afford to pay a market salary, given that they’re startups. With the idea being that hopefully the startup does really well, increases in value, and then employees can participate in an eventual exit of that company, and hopefully make a nice little capital gain there, which is overlaid by the sweetener at the moment of the 50% CGT discount. So, taking that away arguably does make those plans less attractive to startups.

But I guess hopefully we get a bit more clarity in the next couple of weeks once there’s been that consultation between the government and the startup sector to see whether or not that would actually be addressed once those discussions happen.

Laini Bennett: So, with that in mind, is there any point for startups doing things like looking at incentive structures, or issuing new equity, or refreshing their option plans, or should they be holding off until those discussions take place?

Thomas Linnane: I think it’d be worthwhile just pausing on doing anything drastic until we find out a bit more, especially given that there’s been a lot of talk in the startup space, and those discussions are going on between the startup sector and the government. So, we don’t want to have a bunch of these discussions where we’re essentially looking into a crystal ball to figure out what the landscape might be. But as soon as that clarity is released, or there’s further information released by the government, then absolutely it would be worthwhile having those discussions to see how the plans might need to be changed, or whether new plans might need to be put in place.

At the end of the day, it sounds like while the CGT discount is being altered, it’s not being removed in its entirety, so hopefully there’s still an incentive there. But fingers crossed once these discussions happen, it’s made at least equally attractive as it is now to try and attract those key talent into startups, with that being kind of the whole idea of why those startup concessions and those equity plans were put in place in the first place.

Laini Bennett: Okay, thank you. So, James, then, from a numbers perspective, notwithstanding that things could change a little bit with some consultation, how should businesses model the CGT changes? So, for example, should they be talking to someone like yourself, an accountant, to compare before making decisions about asset sales, valuations, or timing?

James Carey: Definitely. The impacts of these rules are going to be pretty widely felt, and I know there is a lot of talk about startups, but there are a lot of longer-established small businesses that will be greatly affected. These rules also change a lot of our traditional tax advice that we would give for people. So, for example, putting the small business concessions aside, the vendor, the person selling a business, normally gets a better tax result by selling the shares in their existing company. Now, the purchaser doesn’t want that because they don’t necessarily want the history, but the 50% CGT discount is better than the money going into the company.

This loss of the discount may actually make it preferable for people to sell the business out of the company. The money goes into the company, you pay tax at 30%, and then you’ve kind of got some flexibility to retain it and pay it out over a period of time. But also just understanding what these rules will do — and it’s not just business, it’s all CGT assets that you might own.

To give another example, I have a client who owns some pre-CGT farmland in and around where I sort of live. And that farmland is zoned farmland. It’s probably worth about $6 million. They have in place an option agreement with a developer who wants to potentially buy that farmland for $25 million, assuming that the property can get rezoned. So there’s an option agreement in place.

If the developer ends up calling that option agreement, it will be after 1 July 2027, and pre-CGT assets are now captured. So if the market value of the property is only $6 million, and they sell it for $25 million, they will now pay capital gains tax at 47%, which is a lot more than paying no capital gains tax. So the impacts are going to be broad. It’s a great outcome for the client if this sale happens anyway, so that’s fine, but it’s certainly changed their thinking around how things are going to flow.

And understanding the indexation is another point. I was just doing some quick modelling before, testing what the government has been saying around, well, indexation can lead to an equivalent discount. They’re sort of saying between 30% and 60%. I used the example of buying a property for $1 million, assuming the same CPI inflation of about an average of 2.7 from the last 10 years. If the property doubled in 10 years, you sell it for $2 million, your cost base has actually been indexed up to something like 1.35, and so you’ve got not a million dollar capital gain, but a $600,000 capital gain, $600,000 and something. So it worked out to be about a 30% discount on your capital gain. So, not as good as 50%, but also not quite as bad.

So it’s great if it’s this long-term asset, but if you’ve got a high-growth startup, for example, that doesn’t get the benefit from the indexation, or your startup injection was $100 into your company and you sell the shares, well, there’s nothing to index.

And just, I guess, final point on the numbers and what Tom was talking about: the small business CGT concessions are unchanged. And the way they work is — let’s just talk about a share sale, because we can go like for like. If you have no other assets as a sole founder, say you own 100% of the company, say the company’s worth $5 million, if you sell the company for $5 million, using the small business concessions, provided you put some money into super and you use the discounts, you end up with about a $940,000 tax bill, so you get $4 million after tax.

If instead you don’t sell, and you grow your company for an extra 2 years or something, and sell it for $10 million, after paying your capital gains tax, you have $5.3 million. So it’s going to really change, I think, the behaviour of people growing businesses about, well, do I just step off before I hit that $6 million mark, instead of staying to grow, because I won’t capture that much of the upside. So the changes are big, and use a spreadsheet and speak to your accountant.

Laini Bennett: Right. On that point, let’s move on to the next part of the discussion on discretionary trusts. And Tom, let’s start with you. Many SMEs operate with discretionary trusts. What does the proposed 30% minimum tax mean in practical terms for those businesses?

Thomas Linnane: Yeah, so what it means, in a nutshell, is that one of the main benefits of a discretionary trust at the moment is the ability for the trustee to do what’s called income streaming. So, once the trustee gets an amount of income, it’s usually able to make a decision as to which of the beneficiaries under that trust will actually be entitled to that income.

And why income streaming can produce pretty favourable tax outcomes is, maybe there’s an adult child who’s not working at the moment, maybe they’re at uni or something, and so the trustee is able to choose that adult child to distribute a certain amount of income under the trust to that adult child, and because that adult child isn’t working, they’ll have the benefit of the tax-free threshold of $18,200.

So, provided that that’s their only income for that financial year, the trust is able, or the trustee is able, to distribute that money, and no tax is ultimately paid by anyone on that money. So that’s one of the main benefits as to why discretionary trusts are used broadly, not even just trading trusts, which actually operate businesses in their own right, but also discretionary trusts which are used as more passive investment vehicles.

So, now that’s changing quite significantly, and so the trustee will be up for 30% tax on trust income now, even if they do distribute it to any number of the beneficiaries.

Up until now, up until these changes kick in, provided the trustee distributed all of the trust’s income for the financial year, the trustee themselves usually wouldn’t be up for any tax on that income, subject to some exceptions, which we won’t get into. But now, because the trustee is paying tax, any money that is then on-distributed to the beneficiaries would have been already subject to tax, which would then be taxed again in the hands of the beneficiary, but they would receive a credit for any tax that the trustee has already paid. So I guess they’re losing, in some way, that tax benefit of the ability to income stream.

One nuance which came out in the budget when it came to the 30% tax offset is the availability of that offset for corporate beneficiaries, so companies, basically. And so, a lot of times, these discretionary trusts were set up with what’s called a bucket company as a beneficiary, which allowed the trustee to distribute income from the trust into that bucket company. The bucket company would pay tax at the corporate tax rate, and because a company is able to retain its earnings without needing to distribute it to anyone, really, it gave a bit more flexibility there.

So, I think that will need to be thought about as a tax planning strategy moving forward. I feel like that was a not-so-subtle position of the government, and how they feel about things like bucket companies.

So all of that will need to be thought of when it comes to whether or not a discretionary trust now makes sense. There’s still other benefits that the discretionary trusts may offer, things like asset protection benefits — if the people behind the trust live maybe a particularly risky lifestyle, and they want to separate out that lifestyle from certain assets, putting things into a trust still makes sense there. But it does mean that the tax benefits associated with income streaming have been limited.

Laini Bennett: Okay, thank you, I appreciate that. So, James, did you have anything you wanted to add on the discretionary trusts?

James Carey: The government has, for years, talked about doing this, and they finally have, and they’ve just outright said, we don’t like trusts, we would prefer you to use companies. And so they want everybody — and the point about the bucket company is that you can still use a trust, but they no longer want to give you the ability to effectively quarantine income at 30%.

So, it’s been a very useful tool, particularly for trading companies, or where the income is not needed by the beneficiaries, and it’s to be reinvested. Bucket companies are a really nice place to cap that tax, and then you can use that company to invest. I don’t think it completely kills trusts, because the asset protection component of having your investments and whatever in a trust is still useful. The other point is that if the beneficiaries are earning more than $45,000, therefore they’re on the 32% tax bracket, they’re not going to be worse off than before these changes. So there’s still a place for them, but certainly diminished.

Laini Bennett: Hmm, okay. So, should people be — I mean, the government’s talking about maybe granting some sort of relief, which would allow some restructuring away from trusts. What situations would there be where this would be useful to consider?

James Carey: So there is an existing — well, there’s a couple of CGT rollovers that exist, and there is a small business rollover that’s been around for, I don’t know, maybe 10 years. It’s not used very much. What they’re talking about is removing a requirement that you actively run a small business in order to use it, but it will effectively let you say, I’ve got a trust, I want to turn it into a company.

If you have a trading business, and at least in New South Wales, we don’t have stamp duty on the transfer of businesses, and Tom can probably make comment on that. I think in other states there are. But if you have a trading business, you might prefer to turn it into a company, because then you have that benefit of using the 25 or 30% tax rate.

So, if you have a large long-term investment trust holding properties and various other things, you may not look to restructure, because you still get the 50% CGT discount currently up until 30 June 2027, and that discount is available until you eventually sell it, but capped at 30 June, get a valuation, and then it’s indexed from that point onwards. So there is still some benefit there, plus you don’t want to necessarily trigger stamp duty if you’ve got properties and you’re changing entities. So, I think again it’s going to be a lot of advice with your lawyers and your accountants.

Laini Bennett: Speaking of lawyers, Tom, is there anything you wanted to add to that before we move on?

Thomas Linnane: The only point I’d make, just to close the loop on the stamp duty point, I fully agree there, and different states do it differently. For example, Queensland, and off the top of my head, I think WA, just as an example, do still impose duty on business sales or business transfers. So, I guess this would need to be overlaid with that duty advice of, yes, okay, from an income tax perspective, maybe there’s relief in terms of restructuring out of the trust into another structure, like a company.

Certain, or at least I think most, states and territories have what’s called a corporate reconstruction relief when it comes to stamp duty, so as part of this, this would need to be overlaid if it was a business transfer, whether that relief might be available, but we’d need to consider that further. But then for other investment assets, like real property or shares and the like, we’d need to consider that in more detail, particularly because — and this’ll come out in time once the government actually releases more draft, or any draft legislation about how its proposed rollover is going to work.

Things like ownership of the new structure: most of the rollovers that already exist require that the new structure that is being set up has the same ownership. So I’m interested to see whether that’s going to be different for this rollover, and how the ownership of, say, the company that’s incorporated as a result of the restructure of the trust, whether there’s a requirement that it will need to be owned by the trustee, or whether there’ll be some flexibility there.

Laini Bennett: Cool, thank you. Let’s move on, Tom, to talk about the electric vehicle FBT exemption rollback. The exemption’s been really popular since it was introduced. It’s increased the uptake of EVs, it’s given employers alternative ways of remunerating staff. What are the changes to the EV FBT exemption, and what do you think they’ll mean for business?

Thomas Linnane: Yeah, so there’s a couple of changes there, and there are some transitional arrangements that have been put in place to not effectively pull the rug out all at once. But at the moment, how it works is, provided that the car meets certain conditions, and provided it’s under a certain value, which is tied to the luxury car tax threshold, if an employer provides an electric vehicle to an employee through some kind of direct arrangement, or even through things like a novated leasing type arrangement, the employer isn’t going to be subject to fringe benefits tax on that arrangement, even though there’s a car benefit being provided.

So, those arrangements that are already in place, from what we understand, they’re not going to be affected by the changes, so those will continue to be exempt from FBT, up until 1 April 2029, which is going to be the start of the 2030 FBT year.

Provided that the car that’s provided to the employee still meets those conditions of being an eligible electric vehicle, and has a value of under $75,000 or more, it will still be eligible for a full exemption. But anything above that will be subject to a reduced exemption, so a 25% discount.

So, it means that in providing these benefits to staff, if it’s a policy that they do it on a wider basis, or even if an employee just comes and asks — which happens quite frequently; we have a lot of calls where the only reason it’s ever come up is because an employee of one of our clients has gotten some spam email about a novated lease for an electric vehicle, and they’re keen to explore it — so just thinking through whether it’s going to be an attractive incentive for the business moving forward, which will need to consider things like the actual value of the proposed vehicle under the arrangement. So if it’s quite an expensive vehicle, maybe it’s not worthwhile.

So, it’ll change things there, particularly because the fringe benefits tax rate is the highest rate of 47%, so it’s not an insignificant tax. So all of a sudden, a lot of these arrangements, which weren’t subject to FBT, could re-enter the FBT net, so business will need to think about whether, if they have been adopting this as a remuneration strategy, it’s still viable once the new changes kick in.

Laini Bennett: Great, thank you, Tom. Lots to think about for EVs there. James, let’s turn our attention to some of the tax wins. So, maybe there are a couple of positive things that have come out of the budget on hopes, including the permanent instant asset write-off and the return of loss carry-back. Could you start by briefly explaining what these are, and which businesses are most likely to benefit from them?

James Carey: Okay, so this will be a very short section on business wins. So small businesses — and I would need to check the threshold, because there’s a bunch of different thresholds. It’s either $10 million or $50 million of turnover — small businesses can instantly claim a deduction for an asset that costs less than $20,000. Anything greater than that, or if you’re a large business, anything greater than $300, you have to depreciate over the effective life.

So, this $20,000 cap has been in place for a number of years. Over COVID, it went unlimited, it was $150, it was kind of jumped all over the place, but the default setting without this was $1,000 is the cap. And so, every year, the governments have just been rolling it forward and going, oh, we’ll allow it again. So, they’re just making it permanent. It’s kind of just what we’ve been doing anyway, so that’s nothing too exciting.

Laini Bennett: Nothing too exciting, okay.

James Carey: The other thing is actually a useful tool. So this is a loss carry-back rule. And what it means is, if you have a company that makes a profit in year one, it pays tax on that profit, 25%, whatever it is. If it then has a loss in year two, because of growth or whatever, what normally happens is, well, that loss carries forward until you eventually have a profit, and then that profit is soaked up by the loss, subject to a bunch of other things, and then once you’ve used up all your losses, you start paying tax again.

So, the loss carry-back rule, I think, first came in 10 years ago, and it only lasted 2 years before it got repealed. And the premise is, you pay tax in year one, you pay tax in year two, you make a loss in year three, you’re allowed to use that loss to claim back any tax that you’ve paid in the prior two years, so there’s a two-year threshold. So it’s really helpful if you’ve got a business that sort of is fluctuating, or investing in growth, or whatever happens — you get some of that tax that you’ve paid back. There’s some extra rules around you can’t have then paid out fully franked dividends and gotten that tax benefit from the tax credit, but it’s a really useful thing if you have a fluctuating business.

There is an additional benefit for startups, which is like the startup loss carry-back rule, which I don’t think kicks in until the 1st of July 2028, but what that says is, if you’re a startup in your first two years, I think, and you run a loss, you can actually cash out that loss. Now, it is limited to the amount of withholding tax you pay on wages, or FBT that you pay on fringe benefits. So, for example, you might have a $100,000 loss, that’s actually worth $25,000 of future tax saved. If you paid $100,000 worth of salary, and as part of that salary, you paid $25,000 to the ATO as a withholding tax, well, you have enough credits to claim the full loss back. So it’s kind of neat for startups to kind of help get them through.

I think if you’re claiming R&D, it’s probably the R&D’s cashing out the loss anyway. So, yeah, it’s kind of nice for those early-stage companies, but again, it’s not going to hugely change the landscape, I think.

Laini Bennett: You touched on R&D incentives there. Is there anything that’s going to change for these under the proposed reforms, specifically?

James Carey: Yes, so R&D has been one specific thing that they have made some moderate changes to. So, the first is they have increased the rebate amount by 4.5%, so effectively you get a little bit more money back, you get a little bit more tax benefit. For every dollar that you spend, you get an extra 4.5% cents back, either as a non-refundable tax credit if you’re a large business, or as a refundable tax credit if you’re a loss-making, smaller business.

So that’s one. That seems good, but then on the other hand, to give with one, take with the other, they’ve removed the eligibility to claim what’s called supporting R&D activities. So, if you make an R&D claim, there’s two components. One is the core R&D that meets the requirements of making the claim, which is, it’s technically risky, you’re creating new knowledge, passing all of those tests.

All of the work that supports that, which might be admin overheads, it might be the whatever supporting activities, they used to be claimable, so you might claim 20% of the CEO’s salary, because although maybe he’s not in there doing the R&D work, he’s supporting it with strategy and whatever it is. They’ve more or less said you can no longer claim any supporting activities, and for some claims, it can be quite a big amount, so you kind of get some extra benefit in the higher rebate, but you lose the ability to claim all of the supporting activity.

So that’s quite a big change. The other big one is for older businesses, where you have been trading for longer than 10 years. If you’re a small business, you are no longer entitled to the refundable offset, so you can no longer cash out those losses. And the government’s argument is, well, if you haven’t made money after 10 years, we’re going to stop supporting you with cash benefits.

And maybe that’s a reasonable position. I have some clients who are constantly investing in growth, and they do run at losses, and they have been running for longer than 10 years, and they do get R&D benefits, so this will seriously hit some businesses who have kind of become used to claiming it. But, you know, we just need to manage that now.

Laini Bennett: Fair enough. Some good tips there. Speaking of tips, let’s just talk briefly about end of financial year tax planning before we get to questions, because we can see quite a lot of them coming in. So, with everything that we’ve talked about so far, and just in general, what are the key actions that businesses should be taking before year-end to optimise their tax position, James?

James Carey: James, alright. So, tax planning with the budget, I don’t think it’s really necessarily changed, because they have given a lot of lead time for some of these changes. So a lot of the traditional things that your accountant and tax lawyer would work with you on remain unchanged.

If you have borrowed money from your private company, make sure that you have Division 7A loan agreements in place, or you repay the loans before the tax return is lodged.

If you have multiple entities within your group, and they provide services to each other, make sure those arrangements are documented with proper service agreements. There was recently a case that I’m sure Tom knows the name of, and I’ve forgotten, where — it might have been a real estate agent with a group of companies, was constantly moving, doing invoices between the companies. The ATO said, we’re going to disallow those deductions because they’re not allowed, because they’re not documented. He went to the AAT, or whatever that’s called now, and won. And the tribunal basically said, no, small businesses operate like this, they often know what they’re doing, they will allow it. The ATO appealed it, it went up to the next level, and the ATO won. So, we had a brief moment where we thought, okay, we can, as a small business, relax, but documentation is really important.

If you have a trust, make sure you have your trust distribution resolutions documented before June 30. If they’re not in place by June 30, you don’t have a valid trust distribution, and the trustee pays tax at 47%.

All of the usual stuff around, if you want to prepay interest to get a deduction this year, there’s normal tax planning things that you can speak with your accountant about. Don’t necessarily go out and spend a bunch of money to get a tax deduction if you don’t need the items. Get some estimates. We’re spending a lot of time at the moment meeting with clients, giving them a bit of an estimate, making sure that we’re declaring dividends, all of that sort of usual stuff.

Laini Bennett: Terrific, thank you for that. So, let’s wrap up the discussion with some actionable takeaways. James, why don’t we go first? If you’re a business owner, or founder, or your finance team, what is the one thing after today’s session regarding the budget that they should be actioning?

James Carey: Sorry, was that James again?

Laini Bennett: Why don’t you go first?

James Carey: I think the main action is probably don’t rush to do anything about the budget, because a lot of things get proposed in budgets and never actually end up getting through. I remember, again, 10 years ago, a $500 automatic tax deduction was proposed at a budget, and it’s taken this long, and now they’ve finally said they’re going to make it $1,000.

The Division 296 tax, the $3 million super tax, that was proposed as a tax on unrealised gains. The actual legislation that got implemented removed that because of the outcry. So I think there will be changes, be it for CGT on businesses, CGT on startups; negative gearing probably won’t change. There’s going to be a bunch of things that we just don’t know. So our conversations with clients are, don’t rush and do anything just yet until we see the legislation.

It is probably changing how we might think about structuring new businesses from now, and setting it up in such a way that gives us the flexibility if the rules change. But, yeah, don’t rush is my advice.

Laini Bennett: Okay, thank you, that’s good advice. Tom, what would you like to add to that?

Thomas Linnane: Yeah, it took a lot of the words out of my mouth, so I guess I’d slightly reword and say, don’t rush, but also don’t panic. Given that we have a pretty significant amount of runway, and a lot of balls are up in the air at the moment, it would be worthwhile just taking the time to make sure that no rash decisions are made, while we don’t have the full picture.

But, as more of a broader point, whether the changes come in or not, it still would be worthwhile to think about structuring more broadly, because beyond the CGT changes, circumstances can always change. So it’d be worthwhile having to think about, okay, is my current structure appropriate? Is it worthwhile having a check-in to think about it more broadly? What are my plans when it comes to investment, for a future exit? That kind of thing.

And that can all be overlaid with what’s been proposed, to, as James said, make sure that you have the most flexible and worthwhile structure in place.

I’m going to be a bit naughty and add one more, which is not budget-related, but I’d be remiss if I didn’t at least throw it in somewhere, is: given that we’re coming up to 1 July 2026 quite soon, just make sure that if you haven’t already as a business owner, putting in place steps to make sure that you’re ready for Payday Super.

Laini Bennett: Absolutely.

Thomas Linnane: The Payday Super does commence from 1 July, which is now where superannuation contributions are due within 7 business days of salary or wages being paid. There’s a bit more nuance to that, but that’s the broad-strokes effect. So making sure that your payroll systems and software are ready for the change. Making sure that you’ve done your cash flow considerations with your accountants and other advisors to make sure that you’re not going to be negatively impacted from a cash flow perspective. If you are using the ATO Small Business Clearing House for superannuation payments, make sure you transition away from that as soon as possible, because that will be closing from the 1st of July.

So, things like that, which, as I say, are not budget-related, but are certainly very pertinent as we move towards the end of this financial year.

Laini Bennett: Great, that’s a good tip. So, in short, just watch and wait. Let’s see what else is going to be coming out, when they nest the details of the budget outcomes. Don’t rush to make any major decisions until those details come through, and talk to people like Tom and James before you make any major decisions.

All right, so that concludes the main part of our webinar today, and we are going to be coming to your questions in just a second. I have — I should have here James’s contact details for you.

Sorry, I don’t know if they’re appearing… yes, they are.

James Carey: I think they are.

Laini Bennett: Sorry, thank you. So you can reach out to James at these details, and we will be sending these out along with the webinar recording as well. You will also be able to speak to Tom and our team if any questions you might have don’t get covered off today. And an end of financial year checklist, you can download that for free from our resources tab, or by scanning the QR code. That’s a useful tool to have as we approach June. And while our expert guests are answering your questions, you’ll see a poll question pop up. We’d appreciate if you could please answer it.

All right, over to our experts to answer the questions that have been flowing in.

Q&A

Thomas Linnane: Thanks, Laini. I’m just scrolling through to choose a couple to answer. Some of these, I’ll just say at the outset, are very specific, so it might not be within the scope of this session to go into the details of these specific situations. So if we aren’t able to answer your questions, please feel free to sign up for the complimentary consultation. We can see how we can assist.

I might start with one which has actually been front of mind. I’d be keen to get your thoughts on it, actually, James, as well as, I guess, my own thoughts, and it’s all very up in the air at the moment, but the question is: I’m in a high-frequency trading business — I assume they mean shares or similar. I usually trade in and out of the market during the trading days using software that we build and will build. What are the impacts on my current setup, and how can we adapt to the new changes?

So this has been somewhat front of mind, just in my own looking at things on social media and the like, of investors who do invest in frequently traded shares and having to manage things like the cost base indexation and the like when the asset’s being turned over quite frequently. So, do you have any practical tips on how that might work from an accounting perspective?

James Carey: Okay, so, yeah, if you’re running a high-frequency trading business, your revenue would generally always be on revenue account, so it’s not a capital gain, you don’t get the 50% discount, you are always just paying full tax on those profits. If you’re doing it in your own name, you’re always just going to pay the tax at your marginal rate. So, there is no change under this to that structure, assuming that you’re there.

If I had a client that was doing that, a company would seem like a pretty good place to run that business, because the company pays — if you’re actively running a business versus a passive business, and this sounds active, you get the base rate entity 25% tax rate. So, I don’t think these budgets really make any change to this kind of business.

Thomas Linnane: Okay, great, thank you. I’ll answer this next one, which we did touch on in the webinar, but the question is, could you please explain the effects on employee shares?

So, again, this will all harken back to the point that we made around, it’s a bit of a wait-and-see at the moment. But assuming, let’s just say, that nothing changes, then what the tax impact will be for that employee share scheme will really depend on the structure of the scheme itself, because there are a couple of different ways of structuring an employee incentive plan, which are taxed under different parts of the legislation.

One in particular that a lot of startups try and get under is the startup concession, which does have a lot of tax benefits. One of which is, when it comes to things like the 50% CGT discount, you’re taken to have acquired the shares that you get from exercising your options, for example, on the same date that you were granted those options, so it doesn’t actually break the timer for the purposes of things like the 12-month discount when you actually exercise those options.

So, in terms of what it might mean for those types of plans, it’ll be subject to the same rules as other CGT assets at the time of sale, because that’s already how it works. All of the tax that happens under those startup concession plans is dealt with at the time that the shares are sold as part of some kind of exit. So, it’ll look to things like the CPI calculations and the tax that’s payable, as instead of getting the automatic 12-month 50% discount, which will be in place up to 30 June 2027.

The flip side of that is if it’s a different type of structure of your employee incentive plan. So there are other types of plans — for example, the tax-deferred plan, where all of the tax that you’re paying as a result of participating in that plan is already assessed as assessable income rather than as any kind of capital gain. So it means those types of plan structures aren’t really affected by this, because the CGT discounts usually aren’t available anyway in those circumstances.

So yeah, it’ll really come down to exactly what the plan is and what it’s looking to achieve, as to whether or not these proposed changes will affect them or not.

Maybe another one for you, James. So, again, we’ve kind of touched on this in the webinar, but — and I’ll maybe paraphrase the question slightly to maybe pull out a bit more — but there’s a question around discretionary trusts and a bucket company beneficiary of that discretionary trust. So, given the proposed changes, I guess, to both the CGT rules and trust tax, and the offset not being available for bucket companies, what place do bucket companies still potentially have in a tax and asset protection strategy?

James Carey: So, the trust changes don’t kick in until 1 July 2028, so the FY29 year. There are still 3 tax years where bucket companies can be used — the current one, FY26, FY27, FY28.

I have a few clients where we have, just in the last couple of months, been setting up bucket companies as part of a longer-term tax planning, asset acquisition strategy, and they’ve all asked, do we just need to throw it out the door now? And my answer has been, no, because we still have 3 years, so there is still time to get the money in there, or 3 years’ worth of distributions into that, and benefit from the 25 or 30% tax rate, depending on whether the trust income is small business income or passive income.

And I think that these changes, both to trusts and to the capital gains rules, will largely see a big return on investment companies. So, pre the CGT discount being introduced, investment companies were very popular because you were capping tax at the company tax rate, as opposed to the individual tax rate, which was always much higher.

So those bucket companies, although they will no longer be able to receive trust distributions from FY29 onwards, because they’ve deliberately said you’ll pay double tax and potentially triple tax, and there’s some debate about whether it’s 62% or 75%, because we don’t know what the rules — how it’s going to work, but we can no longer receive it. But if you want to be buying long-term capital growth assets, maybe the company’s going to be useful, or you have a bunch of money sitting in term deposits in your own name, well, park that in your bucket company.

I saw somebody else talking about an interesting strategy, because accountants and tax lawyers are always going to try and solve problems, where negative gearing is off the table if you buy a property. But potentially, if I set up a company, and I borrow a million dollars from the bank, and I use that million dollars to subscribe to shares in my company, and my company uses that million dollars to buy an investment property, well, maybe I get a tax deduction for the interest against that investment company.

So, there are going to be loopholes and ways around it until they say, oh, we’re going to stop that, oh, we’re going to stop dividend-only shares, oh, we’re going to stop things. So, it’s just the nature of the tax system being so complex that the legislators will always be playing whack-a-mole with the —

Thomas Linnane: Absolutely.

James Carey: — tax lawyers coming up with workarounds.

Thomas Linnane: Yeah, absolutely. Always some fancy footwork to be done, right?

This question’s come up a couple of times, so maybe we address them all at the same time, but there’s been a couple of questions around the proposed changes to the trust tax — changes which kick in in a couple of financial years’ time, whether they’ll apply to only trusts set up after that time, or all existing trusts, or discretionary trusts, I should clarify, that are already established before then.

So, my understanding is that it does apply to all trusts that are already in place and established after that time. Is that your understanding as well, James, at least from what we already know?

James Carey: So, we’re talking discretionary trusts.

Thomas Linnane: Yes.

James Carey: Fixed trusts and managed investment trusts, they are exempt from these rules. Now, there is one little trap that — unit trusts is a type of trust that people often think are fixed trusts, but a default unit trust is not necessarily a fixed trust, so there might need to be some consultation with lawyers to make sure your unit trust is a fixed trust.

But the other exemption was for testamentary trusts, which are created by a will that existed prior to budget night, I think. So those trusts already in existence do not have the 30% minimum tax. However, and this has kind of been in the press about death tax, blah blah blah blah blah, but what they’re saying is, any testamentary trust created after budget night is subject to this same 30% minimum tax, and any existing — sorry, to clarify — any existing discretionary trust is subject to this 30%. It is not grandfathered, it is not quarantined; every trust now has to deal with this.

And to further clarify that, they’ve said that even if you have a will, and it has a testamentary trust in it, the trust hasn’t been created, so provided you die after budget night, your testamentary trust is going to have this 30% tax rate applying to it.

Does that answer the question?

Thomas Linnane: I think so. We probably have time for maybe one more.

So, the question is, what do I do as a sole trader who’s been running an agency to transition to a company structure to minimise my CGT in the transfer? I’m also launching a startup with an MVP, but not yet incorporated. How do the CGT changes impact a business launch in 2026 that then sells for, for example, $100 million in 2030?

Well, I guess there’s a few threads to pull in that one, but I’d say in terms of the restructure component, there’s already a couple of solutions that you could look at to deal with the potential CGT impact of doing a restructure like that.

There is the small business rollover relief that James spoke about earlier in the webinar, and there’s also another type of rollover relief which we could look to as well, which, if either of those are available, it would allow the taxpayer to completely disregard any capital gain now, and it would be deferred to a later point in time. So there’s already ways around doing restructures like that, that, provided the conditions are satisfied, won’t result in a tax bill at this stage.

In terms of the potential growth of the business and what that might look like for a potential exit in a few years’ time, I might defer to James in terms of how that might all wash out with the CPI calculations.

James Carey: So when you use those rollovers, the shares that you get tend to inherit your cost base, which for a startup is nothing. So, you can’t index — applying 5% inflation to nothing is going to be nothing. Or, if it’s $10, or $100, or whatever it is.

So, effectively, if you sell the business for $100 million, and you’re selling the shares in the company, you’ll probably be paying very close to 40% tax on that sale. If the company sells the business, well, the $100 million goes into the company, and it pays $30 million. You’ve got $70 million in the company, but if you want to get it out all at once, you’ll end up paying top-up tax.

So, I think we’ll, as I said before, we’ll see a lot of probably business sales, rather than share sales.

Yeah, anyway, we’ll see. Brave new world.

Thomas Linnane: Yes, that’s right.

Laini Bennett: Indeed. Gentlemen, thank you so much for your knowledge and practical examples that you’ve given today. There’s still a lot of questions. Sorry that we didn’t get to everything. I’m sure many of you still have questions on the back of what’s come out in the budget. Remember, you can claim your complimentary consultation with LegalVision. We will be in contact with you, giving you a call this week. We’d love to hear from you. If you want a consult, you can pop your details into the survey that comes up at the end, and complete the survey with feedback. That would be very helpful as well. Please join us for our next webinar. And again, gentlemen, thank you so much for all your time and knowledge today.

James Carey: Thank you.

We appreciate your feedback! Request your free consultation now.