In Short

- Venture debt provides startups with growth capital without immediate equity dilution.

- It typically involves term loans, revolving credit facilities, or revenue loans, often accompanied by warrants.

- Suitable for startups confident in their growth trajectory and future equity raises.

Tips for Businesses

Before pursuing venture debt, ensure your corporate structure is appropriate, obtain necessary approvals, and understand the terms, including interest rates and security requirements. Consult legal professionals to navigate the complexities and align the financing with your business goals.

On this page

- What Is Venture Debt?

- Why Venture Debt?

- Venture Debt Vs. a Traditional Bank Loan

- Is Venture Debt Suitable For My Startup?

- When Is It Appropriate to Use Venture Debt?

- How Does a Venture Debt Deal Work?

- Interest

- How Does Security Work?

- Types of Security

- How Do I Prepare for Taking on Venture Debt?

- Do You Have the Right Corporate Structure?

- Do You Have the Right Approvals in Place?

- How Do I Deal With Repayment and Default?

- Key Takeaways

Most startups are cash hungry. Although a small number of startups do grow without raising external capital, they are few and far between. As Paul Graham famously noted, “Startup = Growth”, and rapid growth is usually difficult to achieve without initially running a business at a loss. There are two main types of capital a company can raise: debt and equity. Traditionally, startups have raised equity capital, and this often makes the most sense for a startup, particularly during its early stages. However, there are circumstances where borrowing money can make a lot of sense for a startup. That type of debt financing is known as ‘venture debt financing’.

This guide is designed to provide startup founders with the information they need to determine whether raising venture debt makes sense for them.

What Is Venture Debt?

Venture debt is a type of debt provided by certain types of lenders, both individual angel investors and funds, to fast-growing startups, early stage companies and scale-ups. This financing option can be suitable for growth capital.

Term Loan

A term loan is similar to a traditional bank term loan. As the name suggests, by the end of the term, the borrower must have repaid the loan in full, including the principal loan amount and all accrued interest.

Interest will accrue on the outstanding loan amount. Term loans may attract an interest-free period, otherwise, the borrower will be required to make regular interest payments during the term of the loan. Venture debt lenders generally offer interest rates of 8% – 20% per annum, depending on factors such as the:

- warrants offered to the lender;

- credit profile of the borrower; and

- term of the loan.

The borrower may have to repay the principal loan amount in regular instalments throughout the term of the loan, or via one large ‘balloon’ payment at the end of the term. A balloon payment is a large payment due at the end of the loan term to repay all outstanding principal and interest.

Revolving Credit Facility

A revolving credit facility is similar to a credit card. You will:

- negotiate a maximum withdrawal limit with your venture debt lender; and

- borrow and repay money from time-to-time, as long as you never reach the withdrawal limit.

There is generally not a fixed time for repayment of amounts borrowed under the facility, although interest will accrue on amounts you have borrowed. You may also need to pay an annual fee, also known as a line fee, to your lender, even if you do not borrow under the facility.

Revenues are unpredictable, especially when you are growing your business. A revolving credit facility can help you cover your outgoing expenses, even if your business’ cashflow is strapped in a particular month.

Like all forms of venture debt, a revolving credit facility can help you establish and manage your company’s credit history. On any given day, you can withdraw only as much cash as you know you can pay back. Unlike a term loan, you do not have to make long term projections of your company’s cash flows to determine whether you can repay what you borrow.

Revenue Loan

A revenue loan is an interesting hybrid between debt and equity. It is a form of debt like a traditional interest-bearing loan, but rather than fixed interest payments, the repayment is tied to the borrower’s turnover.

Although the rate can vary, it is typically between 3% and 5% of the business’ monthly revenue.

But, this flexibility comes at a cost. Investors will typically only offer revenue loans to high growth companies that are expected to quickly repay the loan. If this happens, the effective interest rate is generally higher than a traditional, interest-bearing loan.

Usually, the total amount the borrower must repay is set as a multiple of the principal loan amount and is between two to three times the principal loan amount.

Why Venture Debt?

For the right type of borrower, venture debt can be a cheap and quick way to access money. If you have a high degree of confidence in your company hitting its growth milestones and raising future capital through equity rounds, you should consider venture debt.

It is worth noting that venture debt is not the only type of debt that a fast growing startup can potentially access. There are two other potential options: accounts receivable financing and equipment financing.

If you are profitable and have a large number of customers on payment terms, accounts receivable financing could work for you.

If your business makes use of relatively expensive equipment, then financing the purchase of it with an equipment finance loan could be a great option.

Continue reading this article below the formCall 1300 544 755 for urgent assistance.

Otherwise, complete this form, and we will contact you within one business day.

Venture Debt Vs. a Traditional Bank Loan

To better understand venture debt, it is worth comparing a standard venture debt structure to a typical bank loan.

Because venture debt lenders are generally lending to unprofitable companies and are not taking personal guarantees from founders, the risk profile of a venture debt deal is much higher than that of a traditional bank loan. This means venture debt investors seek higher returns than banks, in order to offset their risk. For instance,

venture debt lenders may seek to sweeten their deal with:

- a high interest rate;

- security over all your company’s assets; or

- the option to buy equity in your company at a discount.

| Venture Debt | Bank Loan | |

| Security | Venture debt lenders generally do not require either personal guarantees or mortgages over personal property from the founders. Instead, they take security from the company itself. This is more attractive to (and less risky for) founders. |

The startup founder will likely need to offer a personal guarantee and mortgage their personal property as security. Most banks will not lend to a fast-growing company that is still loss-making without this security package. |

| Warrants (or ‘Equity Kickers’) | A warrant is a right to purchase shares in the startup at a set valuation. If the startup does well, the warrant will enable the venture debt lender to participate in the equity upside. | You are not generally required to give warrants as part of a traditional bank loan. Banks are not interested in taking equity stakes in startup companies. |

| Interest Rates | Venture debt interest rates can range from 8% – 20% per annum. This is a higher interest rate than a bank, designed to offset the risk of venture lending. |

Bank loan interest rates are typically much lower than venture debt interest rates. They can range from 4% – 15% |

Is Venture Debt Suitable For My Startup?

If you raise money through equity, you are selling an ownership share in your company to your investors. Those investors will then share in any increase in your company’s value through their ownership share. Venture debt does not require you to sell ownership in your company upfront. Instead, you borrow money from investors with a promise to repay it.

There are six questions to consider in determining whether venture debt is suitable for your startup.

1. How Much Dilution Do the Existing Shareholders Want to Take On?

When raising an equity round, a startup generally issues new shares in the company to new investors, meaning existing shareholders end up with a reduced portion of the company post-round. This reduction is called ‘dilution’. The main reason venture debt is attractive to many founders is that it can reduce the amount of dilution that existing shareholders take on in a funding round.

2. Do You Want to Retain Board Control?

Because venture debt investors do not take a significant ownership stake in your company, they generally seek less control over your business operations than an equity venture capital fund does.

Both venture debt and equity venture capital will place restrictions on a founder’s ability to run their startup. Regardless of which one you choose, your investors

will influence the way you run your business. With an equity investor, that influence may be more direct and significant, particularly if they hold a board seat.

What restrictions can a venture debt investor place on the running of my business?

- Board Meetings: If you have an equity investor on your board, they will be present at your board meetings and can have a direct say in your business decisions. This may be useful if that investor offers valuable advice and guidance. However, if they disagree with your decisions, and you do not value their input, this can be problematic.

- Business Obligations: If you have to comply with certain obligations as part of your venture debt arrangement, you may be indirectly constrained in how you run your business. For example, you may need particular systems in place to be able to meet your reporting obligations. Or you may be restricted from making certain business decisions (e.g. spending money) if it would put you in breach of your financial covenants.

3. Is It a Good Time to Value Your Company?

When seeking venture debt, you are not required to have your company valued.

This is not the case for equity capital, which establishes a valuation for your startup. This occurs because investors set a new share price when they buy shares in your company. In some instances, this can be beneficial, especially if your company has grown significantly since its last raise.

However, some companies may not be at a stage where they want to set a valuation. If you are exiting a period of high growth and transitioning to break even, you may be staring down the barrel of a down round and want to avoid an equity raise – which is where venture debt may be attractive.

4. Do You Need Access to Cash Quickly?

Venture debt can be an advantageous option if you need cash fast. It can be arranged more quickly than equity capital, given that you are generally only dealing with one lender (versus many shareholders).

The due diligence process is also less involved than that of an equity capital raise as the investor will become a secured creditor as opposed to a shareholder in the business. The flip side of this is that your company will have to hit a few key benchmarks in order to be able to access venture debt, such as generating substantial cash flows and having a limited amount of existing debt.

5. Do You Need to Build Credibility?

Successfully securing venture debt can help boost your company’s credibility. Demonstrating your ability to repay that debt is also important, not only to traditional lenders – who you may need to rely on for funding in the future, but also to regulators such as the Australian Stock Exchange (ASX), particularly if you are aiming to list your company.

6. How Can a Company Assess Whether It Is Ready to Take on Venture Debt?

Venture debt is not right for all, or indeed most, startups. Remember that your startup is borrowing money, often a significant amount, which means that you have an obligation to repay it and if you do not, there are severe consequences.

The consequences of taking on venture debt at the wrong time can be catastrophic. Most early-stage startups are not ready to take on venture debt; you generally need significant cash flows, significant assets and an established customer base. You will have a better chance of raising venture debt if you have existing venture capital funding, because:

- the venture debt lenders can piggy-back off the venture capital investors’ due diligence;

- it generally means you are more established; and

- those existing venture capital investors may be a future funding source if you need extra money to pay back the venture debt.

When Is It Appropriate to Use Venture Debt?

Venture debt is a beneficial alternative or complement to equity financing, as it involves less equity dilution, less loss of control, and less time spent capital raising.

There are three scenarios when venture debt may

be appropriate:

1. At the Same Time as an Equity Round

If you are already conducting a round, you can supplement the equity with venture debt. This is the best time to raise venture debt as the company’s materials and management are available and the lender has the positive signal of

investors putting money in. All this allows the borrower to negotiate the best terms.

This is most suitable for companies that are:

- making over $3M in revenue;

- burning significant cash; and

- want more capital without excessive dilution (for example, you could raise a $5M round composed of $3M of equity and $2M of venture debt.)

2. Between Rounds

If you need capital but believe you are approaching a major value inflection point (i.e. a key turning point in your business) and are reluctant to do another capital raising round, venture debt can give you the additional runway you need to achieve more favourable terms.

It has the added benefit of not needing to be paid back at the next round. This type of loan is suitable for companies with up to $5M in revenue, a medium amount of burn and strong existing investors.

3. During Later Rounds to Replace Equity

If you are a later stage company with $5-10M of revenue and a low burn (less than 10% of revenue), venture debt can entirely replace equity financing.

It also offers significantly less dilution for founders. For example, following its Series C fundraising round, Dropbox transitioned to venture debt and the final two rounds of capital raising had no equity. This formed two thirds of Dropbox’s total US$1.7B capital raised. At IPO, Dropbox’s founders owned 36% whereas Box’s founders, which did not use venture debt, held less than 6%.

How Does a Venture Debt Deal Work?

Venture debt involves more than just paying back the amount you borrow. For starters, interest will accrue on the loan. You will also generally have to issue warrants to the venture debt lender as part of the deal. It is important to get your head around these concepts, and what they mean for your business and your ownership of it.

Interest

Interest accrues on the outstanding principal loan amount. The rate of interest will be a point of negotiation between you and your lender. The riskier the loan, the higher the interest rate.

- The interest rate will also vary, depending on:

- the term of your loan;

- the type of loan; and

- whether your rate is floating or fixed.

A floating rate is linked to a benchmark rate, and will change every time that benchmark rate changes.

When calculating how much you can borrow, you need to factor in how much interest you will be paying. If a lender will only lend to you at a high interest rate, you may not be able to borrow as much money as you need. All things being equal, the greater the amount that you borrow, the greater the amount of interest.

If you know that you will not have considerable cash flows in the first few months post drawdown, but anticipate that your cash flows will increase later on, you may be able to negotiate an interest-free period with your lender, or a balloon payment.

A balloon payment is a good way of deferring payments. However, it often comes at a higher cost (i.e. a higher interest rate).

Some lenders will let you capitalise the interest. This means that you do not have to pay the interest amount when it is due. Instead, it is added to your total amount borrowed. Interest will accrue on the amount you borrowed initially, plus the amount of capitalised interest.

Other lenders may grant you an interest-free period, which means no interest accrues or is payable during this period. Lenders offer this feature to attract borrowers. For startups, this may be the clincher in the deal as you may not have enough cash to pay interest from the get-go.

How Does Security Work?

Venture debt lenders will typically want to take security over some – or all – of your company’s assets. Security helps to reduce the risk that the lender will not get their money back if the company defaults on the loan.

When you grant someone security over an asset you own, you give them certain legal rights over that asset. Those rights include the power:

- to take possession of the asset;

- to sell the asset; or

- to use the sale’s proceeds to repay the loan if you fail to repay.

For this reason, security is often a condition of a loan. The most recognisable form of security is a real estate mortgage. As a condition of a home loan, a bank will take security over the newly purchased home.

Generally, if you grant security over an asset, your right to deal with that asset will be restricted. For example, you may not be able to sell it, or grant security over it to someone else, without the lender’s prior consent.

Types of Security

All Asset Charge

Most lenders will ask the company to enter into a General Security Agreement (GSA). Under a GSA, the company grants the lender security over all its assets. So long as the company meets its loan repayments, it will still be able to deal with its assets in the ordinary course of its business.

If the company defaults on the loan, the lender will have the right to appoint a receiver to take control of the company’s assets and manage or sell them in order to recover the loan. The lender can usually only recover the outstanding loan

amount plus its enforcement costs.

For example, if you owe your lender $300,000, and you have $500,000 of equipment, the receiver may sell equipment up to the value of $300,000 and use the proceeds to repay the lender. Once the lender has received its $300,000, the receiver will have completed its job and will give the company control over the rest of its assets.

Specific Security Agreement

Other lenders may ask the company to grant them security over specific assets only. Equipment financing and accounts receivables financing are both examples of financing which require security over specific assets.

- In equipment financing, the borrower grants the lender a specific security interest in the equipment which is being financed by the loan.

- In accounts receivable financing, the borrower grants the lender security over the accounts receivables (i.e. the money that is due from the customers).

Most venture debt deals, however, will be structured with a GSA, as this is much simpler to manage, and ultimately is better security for the lender.

How Do I Prepare for Taking on Venture Debt?

Taking on venture debt is a big decision and comes with significant responsibilities (remember those monthly interest payments!). So it is critical that you carefully consider whether or not it is right for you. Once you have decided you want to go ahead, the next step is preparing your company to take on venture debt.

Do You Have the Right Corporate Structure?

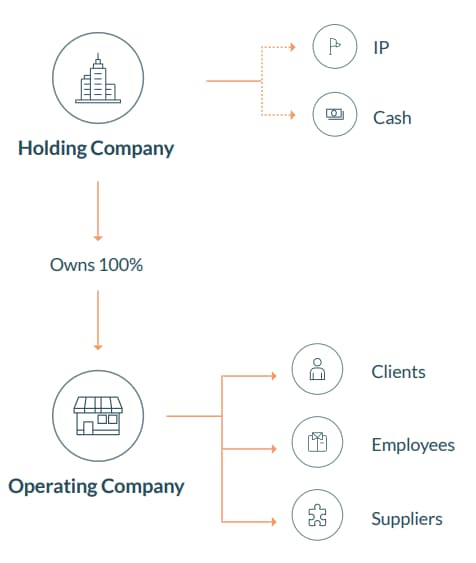

A company structure is the correct vehicle to use for borrowing venture debt. If you already operate through a company, then you are off to a good start. The next question is whether you should put in place a dual company structure.

Dual Company Structure

A dual company structure involves a holding company that owns 100% of the shares in a subsidiary operating company.

The holding company will generally be the entity to borrow the venture debt, as well owning the startup’s valuable assets, such as cash and intellectual property. The subsidiary operating company is the entity that enters into contractual arrangements with clients, suppliers, contractors and employees and therefore carries the operational risk/liability of the business.

A dual company structure often makes sense, because it helps to protect the startup’s assets from the operational liabilities faced by the operating company.

Whilst a dual company structure is great from an asset protection perspective, there are drawbacks. You will need to incorporate (and maintain) two companies rather than one, which is most costly and administratively burdensome than just using one company.

There are also some limited instances where the holding company can be held responsible for an operating company’s action/inaction, such as fraud or other improper conduct, or if the companies are found not to be under separate management in the event of liquidation.

If you do not feel like your business faces huge operational risks, then you may prefer to protect your business by other means, such as taking out appropriate insurance and ensuring that your contracts are robust and limit your liability as much as possible.

Do You Have the Right Approvals in Place?

Taking on debt is a huge decision. You will likely need approval from your company’s directors, and potentially your shareholders depending on your constitution or shareholders agreement. Your venture debt lender will want to see evidence of these approvals, because if you have not obtained them, the transaction may be invalid.

How Do I Deal With Repayment and Default?

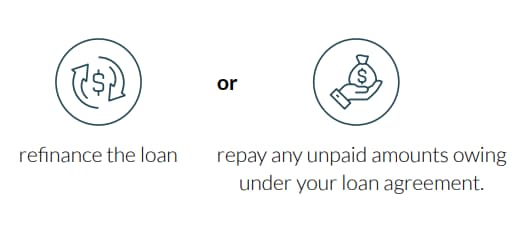

Your loan will have a term (i.e. the final date on which you have to repay any outstanding money due under the loan agreement). This date is also known as the maturity date. It is important to determine what your plan of attack will be on the maturity date, particularly if you have to repay a large amount. You have two options:

Refinancing

Refinancing means you will choose another lender (or possibly the same lender) and borrow at least enough money to repay any unpaid amounts owing under your original loan. You will use this new cash to repay your original lender.

The terms of your new loan may or may not be the same as your original loan, depending on what you negotiate with your new lender and how much money you need.

Your new lender does not necessarily need to be a venture debt lender. Your business may have grown and built its credibility and you might be able to borrow at a cheaper rate from a bank to refinance the venture debt loan.

Repayment

Repaying may be a better option for you if:

- you have repaid most of your loan during the term, and only have a small final repayment to make;

- you are planning on selling your business, either through an IPO or trade sale. The money from your exit can be used to repay your loan;

- your business’ cash flows have improved, and you have enough cash on hand to repay your loan; or

- you have completed another equity capital raise and the proceeds are enough to fund your desired runway and to repay your loan.

What Happens if I Do Not Repay?

You may end up (although it may not be by choice) not repaying your loan on maturity. If this happens you will be in default. You will also be in default if you fail to meet any scheduled repayments during the term of your loan. If you have a good relationship with your lender you will hopefully have discussed your deteriorating cash position early on. Most lenders do not want their borrowers to default. They will do their best to help you get back on track with your repayments.

If, despite everyone’s efforts, you still end up in default, you need to be prepared for some new challenges.

Default

In the scenario where you end up in default, this means all the entire amount of money you borrowed (to the extent it remains unpaid) is due immediately. Any accrued but unpaid interest also becomes payable immediately (even if you are not yet at the maturity date).

Failing to repay your lender can be catastrophic to your business. Nevertheless, it is relatively unusual for a venture debt lender to push a borrower into receivership. It makes much more sense, in most cases, for the lender to work with the borrower to restructure the loan.

Key Takeaways

There has never been a better time to launch a startup in Australia. The ecosystem has come on in leaps and bounds over the last few years, and international successes such as Atlassian and Canva have brought startups into the mainstream.

A key plank of this growth has been our venture capital industry. Our friends at Blackbird Ventures, AirTree and SquarePeg have been critical to the funding of some of Australia’s most successful startups. Until very recently, however, only one type of early-stage capital was available to startups – equity capital.

That has now changed. Venture debt is now a legitimate capital option for the right type of startups. Angel investors, as well as funds such as OneVentures, Partners for Growth and Leap Capital are actively hunting for deals.

We are excited about this evolution because we have worked closely with nearly all of Australia’s most prominent venture debt lenders and we know how useful this type of finance can be (after all we have done two venture debt rounds to finance LegalVision’s rapid growth)!

If you have any questions about venture debt or capital raising in general, please get in touch. We would love to chat!

This handbook aims to help startup founders understand the benefits of venture debt, how a venture debt deal works and how to prepare for taking on this form of capital raising.

If your startup is in a high growth phase and looking to extend its cash runway, venture debt can be an ideal capital raising avenue.

Venture debt is a type of debt provided by certain types of lenders, both individual angel investors and funds, to fast-growing startups, early stage companies and scale-ups. Venture debt lenders generally do not require either personal guarantees or mortgages over personal property from the founders.

You can obtain venture debt if you need cash fast. It can be arranged more quickly than equity capital, given that you are generally only dealing with one lender (versus many shareholders).

Venture capital can take the form of equity financing, debt financing, or a combination of both.

We appreciate your feedback! Request your free consultation now.