Summary

- Changing a trustee generally does not trigger capital gains tax (CGT), as the relevant taxpayer is the office of the trustee rather than the individual trustee.

- Stamp duty may apply in New South Wales and the Australian Capital Territory if the trust holds dutiable property; other states generally provide an exemption.

- If a trustee change is so fundamental that it constitutes a trust resettlement, both CGT and duty consequences may arise.

- This article is a plain-English guide to the tax consequences of changing trustees for business owners operating trusts in Australia, prepared by LegalVision, a commercial law firm.

- LegalVision specialises in advising clients on trust structures and trustee obligations.

Tips for Businesses

Review your trust deed before changing trustees to confirm the change is permitted and properly executed. Check whether your trust holds dutiable property in NSW or the ACT, as stamp duty may apply. Ensure the change does not alter beneficiary rights or constitute a resettlement, which triggers additional tax consequences.

A trustee is the legal entity that holds the assets of a trust. Trustees have significant power as they have the authority to distribute trust income, sometimes at their own discretion. Throughout the life of the trust, there may be circumstances that require you to change the trustee controlling the trust. This article sets out the tax implications that may arise as a result of changing trustees.

Does a Change of Trustee Trigger CGT Issues?

A change of trustee involves the transfer of legal title. However, as long as it is done within the scope described in the trust deed, it should not trigger capital gains tax (CGT) consequences. This is because the relevant taxpayer for the trust asset is the office of the trustee, regardless of the identity of the particular trustee from time to time.

Does a Change of Trustee Trigger Duty Issues?

Trustees have legal ownership over the trust assets. Changing the trustee will therefore require a transfer of ownership of the trust assets from the old to the new trustee.

A transfer transaction may trigger duty tax if the trust holds dutiable property at the time of the change. Dutiable property broadly includes:

- land;

- real estate;

- shares in a company;

- business assets; and

- partnership interests.

In New South Wales (NSW) and the Australia Capital Territory (ACT), stamp duty is generally payable on a transfer of ownership for trusts which:

- people establish in those states; or

- hold dutiable property in those states.

In all other states, an exemption is generally available when the duty arises as a result of a change in trustees. This means there should not be any duty payable when changing trustees.

Exemptions

There are some exemptions or concessions from this tax available in each state or territory. The particular rules and requirements differ from one jurisdiction to the next. But generally, you must meet the following requirements to qualify for an exemption:

- you must enter into the trust for the sole purpose of changing the trustee of a trust;

- the transaction must not change the rights or interests of the trust beneficiaries, or terminate the trust; and

- you must have paid any previous transfer duties on all trust acquisitions.

Note that, in NSW, there are limits on exemptions to ensure that continuing trustees cannot be a beneficiary if a new trustee has been appointed (where there are multiple trustees for a trust). Limits may also apply if the transfer is part of a scheme that detrimentally affects the interest of any parties to the trust.

If you do not meet the exemption eligibility requirements, you may have to pay stamp duty when changing trustees.

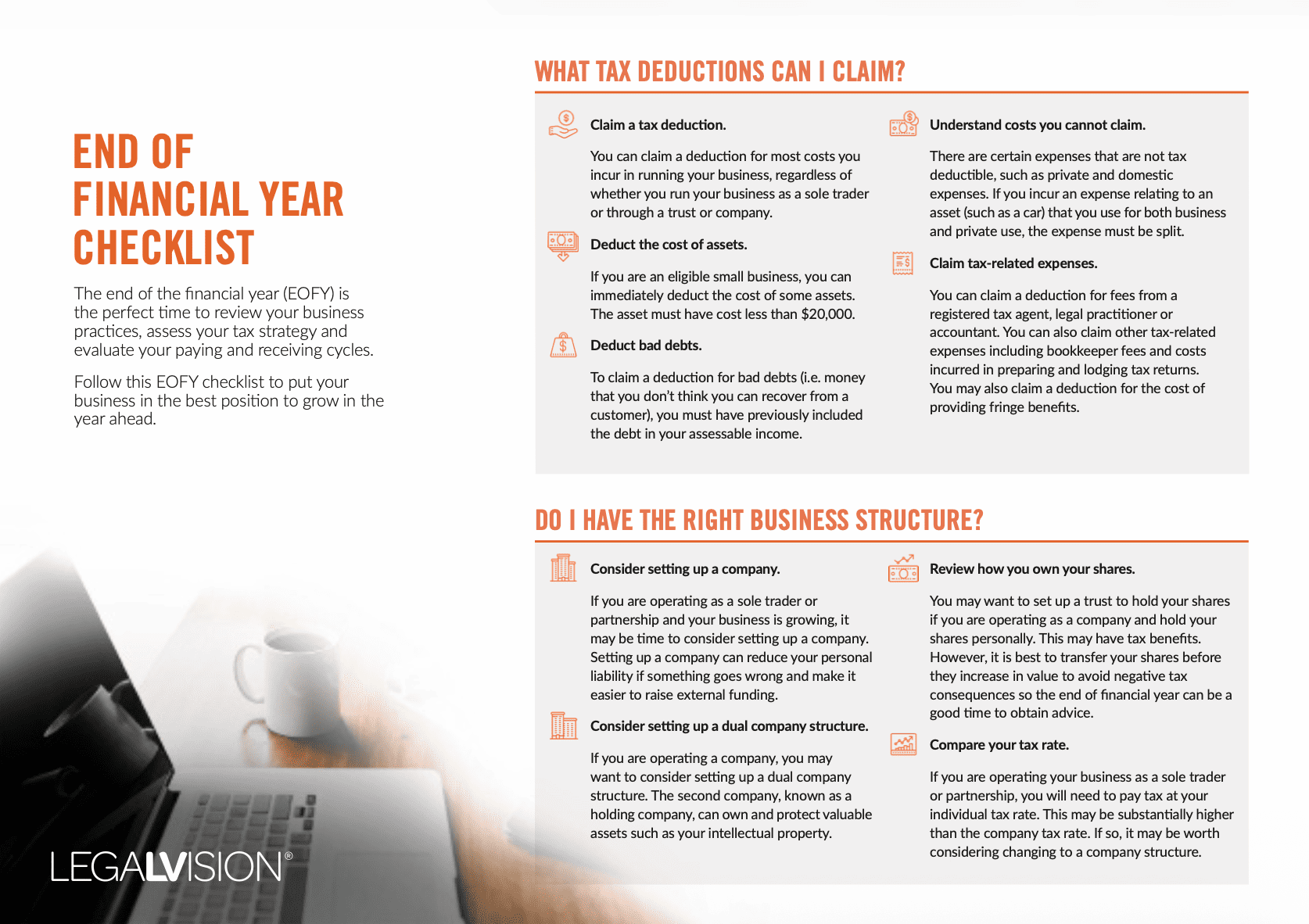

The end of the financial year (EOFY) is the perfect time to review your business practices, assess your tax strategy and evaluate your paying and receiving cycles.

This checklist outlines:

+ the tax deductions your business can claim;

+ whether you have the right business structure; and

+ how to chase up late payments.

Resettlement of Trusts

Regardless of which state your trust is based in, make sure you first look at the trust deed before changing trustees. You need to make sure that:

- the current deed allows for a change of trustees to take place; and

- you follow the requirements and procedures stated in the deed to execute the change.

If the change is considered significant enough that it affects the ‘foundation’ of the trust, it may give rise to a resettlement of the trust. A resettlement effectively means that the relevant changes are so fundamental that the old trust is taken to have ended and a new trusthas arisen. This gives rise to both CGT and duty consequences.

What Happens to Trust Contracts and Bank Accounts?

Changing a trustee also has practical consequences beyond tax. The new trustee will need to update legal ownership across all trust assets. This includes:

- bank accounts held in the trustee’s name;

- contracts where the trustee is a named party; and

- any licences or registrations held on behalf of the trust.

You should notify relevant third parties – such as banks, suppliers, and government agencies of the change as soon as possible. Delays can create legal uncertainty about who has the authority to act on behalf of the trust.

If the trust holds real property, you will also need to update the title on the land register in the relevant state or territory. This is a separate step from executing the deed of change and often involves additional fees.

Planning ahead and preparing a checklist of affected assets and accounts will help you manage the transition smoothly.

Frequently Asked Questions

Does changing a trustee trigger CGT?

Generally, no. A change of trustee transfers legal title but does not trigger CGT, as the relevant taxpayer is the office of the trustee, not the individual trustee.

When is stamp duty payable on a trustee change?

Stamp duty applies in NSW and ACT if the trust holds dutiable property. Other states generally offer an exemption.

What is a trust resettlement?

A resettlement occurs when changes are so fundamental that the old trust ends and a new one arises, triggering both CGT and duty consequences.

What qualifies for a duty exemption?

You must change the trustee solely to replace them, preserve beneficiary rights, and have paid all previous transfer duties.

We appreciate your feedback! Request your free consultation now.