Summary

- An M&A confidentiality agreement should be entered into before any confidential information is exchanged, and must be tailored to the specific transaction, covering the parties, purpose, permitted persons, public announcement restrictions, exceptions to confidentiality, and the confidentiality period (typically one to two years).

- Permitted disclosure is limited to directors, officers, employees, and professional advisors, with co-investors, syndicates, and finance providers potentially negotiated as permitted persons, whilst non-solicit provisions may also be included to prevent the receiving party from approaching key customers, suppliers, or employees.

- Breach of a confidentiality agreement in an M&A context may not be adequately remedied by damages alone, meaning the disclosing party will typically have the right to seek injunctive relief, specific performance, and other equitable remedies for threatened or actual breaches.

- This article is a guide to M&A confidentiality agreements for businesses and advisers in Australia, explaining the key terms that should be included to protect commercially sensitive information during merger and acquisition negotiations.

- LegalVision is a commercial law firm that specialises in advising clients on mergers and acquisitions and commercial transactions.

Tips for Businesses

Enter into a confidentiality agreement before exchanging any commercially sensitive information, even at the earliest stages of M&A negotiations. Carefully review all terms if the other party has prepared the agreement, paying particular attention to the definition of confidential information, permitted persons, exceptions, and the destruction of information provisions. Ensure the agreement is specifically tailored to the transaction rather than relying on a generic NDA, as M&A transactions involve unique confidentiality risks.

On this page

In any mergers and acquisitions (M&A) transaction, protecting confidential information from the outset is essential, and a well-drafted confidentiality agreement (also known as a non-disclosure agreement or NDA) is the first line of defence. Parties will typically enter into one during the early stages of negotiations, before commencing due diligence, signing a term sheet or exchanging definitive transaction documents, to protect commercially sensitive information exchanged while a purchaser assesses the proposed acquisition, particularly if negotiations do not proceed. As confidentiality agreements should be tailored to the specific transaction – including where parties seek to rely on an existing NDA – this article sets out the key terms an M&A confidentiality agreement should include.

1. Parties

The parties to the confidentiality agreement will be the purchaser and the vendor in the transaction. If the person receiving the confidential information (i.e. disclosee) is a holding company with few or no assets, the vendor (i.e. the discloser) may require that a ‘guarantor’ also be a party to the agreement. The guarantor then guarantees that the disclosee (usually the purchaser) will meet the obligations under the confidentiality agreement.

2. Disclosure of Information

The confidentiality agreement will usually define the ‘purpose’ of the agreement. The purpose will include the assessment by the purchaser and its ‘permitted persons’ (discussed below) to evaluate the particular transaction under negotiation.

Continue reading this article below the formCall 1300 544 755 for urgent assistance.

Otherwise, complete this form, and we will contact you within one business day.

3. Permitted Disclosure

The parties to the confidentiality agreement are not permitted to disclose the information provided by the other party, except:

- to ‘permitted persons’ that have been specifically set out in the confidentiality agreement; or

- where the confidentiality agreement expressly excludes the information (discussed below).

Permitted persons are the party’s directors, officers, employees and professional advisors. These parties usually need to know the confidential information to facilitate the transaction process. In circumstances where there are syndicates, co-investors or potential providers of finance (such as banks) to the transaction, the parties may also negotiate them as ‘permitted persons’.

4. Public Announcements

Usually, both parties will expressly prohibit the making of a public announcement about the negotiations of a potential M&A transaction until after the parties have finalised the deal. This prohibition is important because it can have potentially negative ramifications for customers, suppliers and employees of either party if not handled properly.

Further, confidentiality agreements will typically include a clause that requires the parties to consult each other before they make announcements. Where the law doesn’t allow parties first to consult each other, the standard agreement is to inform the other party after making the public announcement immediately.

5. Exceptions to Confidentiality

Confidentiality agreements usually exclude certain information from remaining confidential. It means that any disclosure, under those circumstances, will not amount to a breach of the confidentiality agreement. Typical exceptions include:

- information that is in the public domain;

- information that has been in lawful possession before the date of the confidentiality agreement;

- information that the disclosing party disclosed to the other party through a third party, where that third party was not obliged to keep the information confidential; and

- information that the other party disclosed with the prior approval of the disclosing party.

6. Restraint Provisions

Some confidentiality agreements will also include non-solicit provisions, particularly if the counterparty is a competitor or potential competitor of the discloser of the confidential information. The restraint will usually provide that the party receiving information (and its related entities) must not:

- approach or deal with a major customer or supplier of the disclosing party, other than in the ordinary course of business; or

- solicit the key officers and employees of the disclosing party.

7. Destruction of Information

The disclosing party may require that the party receiving information destroy all the confidential information if the parties terminate negotiations. Destruction will typically include both physical and electronic copies of documents that contain confidential information. However, the receiving party may negotiate with the disclosing party that such destruction provisions do not apply to their internal record keeping, any electronic backup storage or professional record keeping.

8. Termination of Confidentiality

The disclosing party will usually aim to seek from the party receiving the information the maximum possible confidentiality period. The typical period for a confidentiality agreement is between 1–2 years from the date of the confidentiality agreement. In some transactions, the parties may agree that the confidentiality agreement will terminate upon the completion of the merger or acquisition contemplated under the agreement.

9. Implications of Breach of Confidentiality

It is common for a confidential agreement to provide that damages may not be an adequate remedy for breach of the confidentiality agreement. The disclosing party will have the right to apply for an injunction, specific performance and other relief for a threatened or actual breach of the confidentiality agreement.

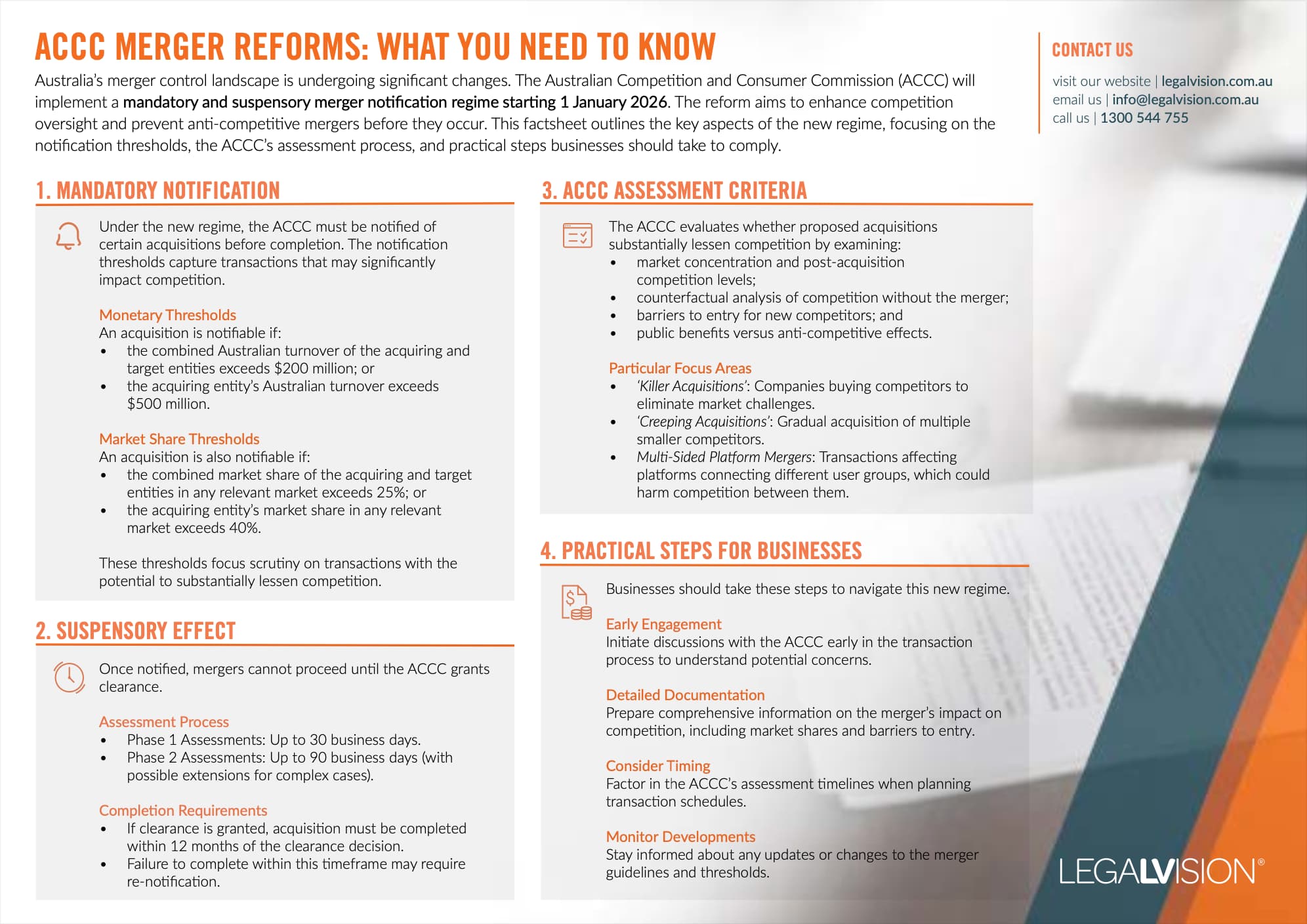

The Australian Competition and Consumer Commission (ACCC) will implement a mandatory and suspensory merger notification regime starting 1 January 2026. This factsheet outlines the key aspects of the new regime, focusing on the notification thresholds, the ACCC’s assessment process, and practical steps businesses should take to comply.

Key Takeaways

It is prudent for parties to enter into an M&A confidentiality agreement before exchanging any information during negotiations. If the other party has prepared the confidentiality agreement, you should ensure that you closely review the terms. A confidentiality agreement for an M&A transaction should be specifically tailored for the particular transaction, and it is important that you carefully review any terms before you enter into such agreements.

If you are entering an M&A agreement, LegalVision provides ongoing legal support for all businesses through our fixed-fee legal membership. Our experienced mergers and acquisitions lawyers help businesses manage contracts, employment law, disputes, intellectual property, and more, with unlimited access to specialist lawyers for a fixed monthly fee. To learn more about LegalVision’s legal membership, call 1300 544 755 or visit our membership page.

Frequently Asked Questions

A confidentiality agreement for M&A should include clear definitions of what constitutes confidential information, the permitted disclosures, and obligations for the return or destruction of the information. It may also include non-circumvention clauses and remedies for breach, such as injunctions or claims for damages.

If a confidentiality agreement is breached, the party responsible may face legal remedies, including injunctions to prevent further disclosure, specific performance to enforce the agreement, and claims for damages caused by the breach.

Permitted persons typically include directors, officers, employees, and professional advisors of the parties. In transactions involving syndicates, co-investors, or finance providers such as banks, these parties may also be negotiated as permitted persons.

The typical confidentiality period is between one and two years from the agreement date. In some transactions, parties may agree that the agreement terminates upon completion of the merger or acquisition contemplated under the agreement.

We appreciate your feedback! Request your free consultation now.